Most couples sit down at the kitchen table to talk about their finances or budget, completely unaware they are walking right into a minefield.

You print out the spreadsheets.

You pull up the banking app.

And within ten minutes, someone is storming out of the room.

Why does this happen so often?

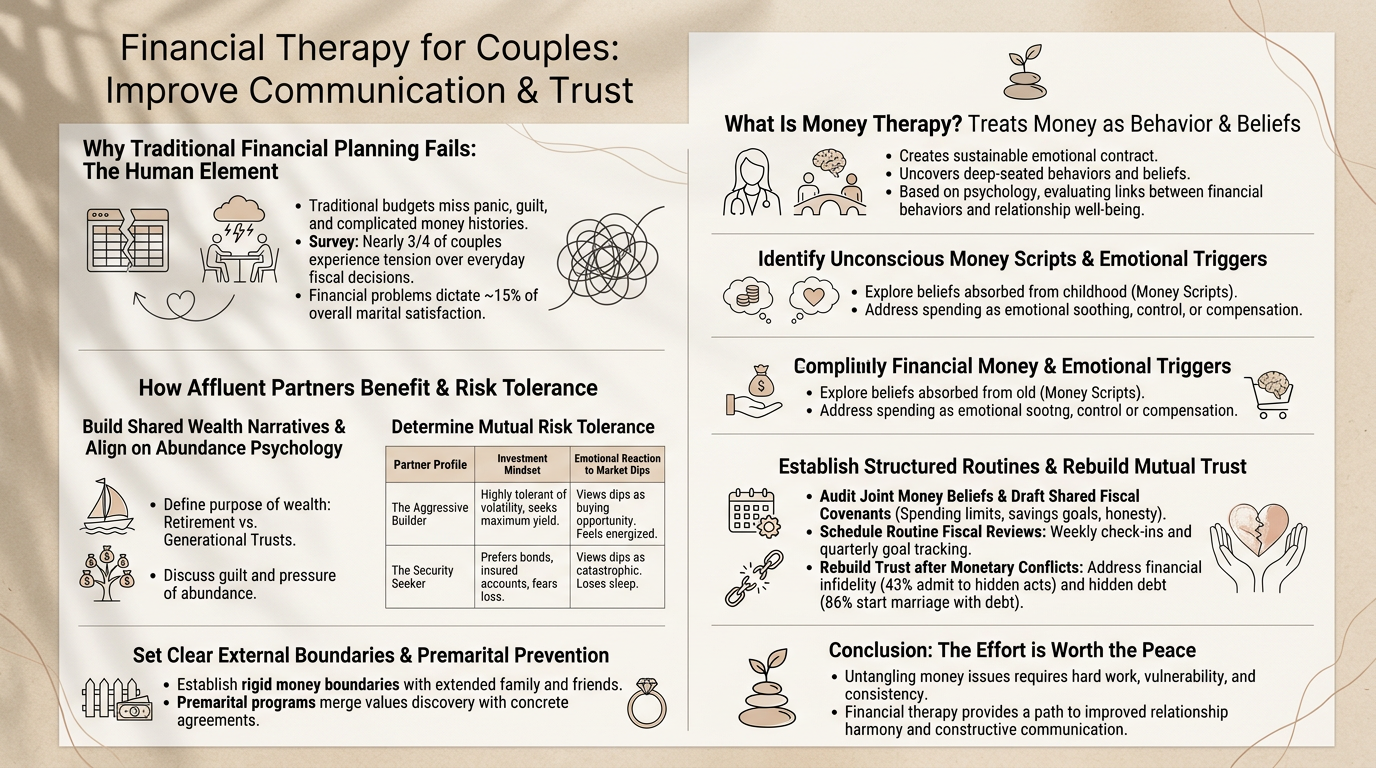

The reality is traditional financial planning completely misses the human element. Spreadsheets don’t account for panic, guilt, or a complicated money history. They just show you the math. But math doesn’t argue with you at 11 PM. People do.

In fact, a survey highlights that nearly three-quarters of married or cohabiting couples experience relationship tension directly related to everyday fiscal decisions.

It takes a heavy toll.

Academic research details that financial problems and subjective perceptions of cash management dictate approximately 15% of overall marital satisfaction levels.

This is exactly why you need more than just a strict budget to survive. You need a behavioral coaching layer on top of your financial plan to make it actually work.

What Is Money Therapy For Relationships?

Financial therapy is an emerging practice that treats money as behavior, beliefs, and relationship dynamics.

It creates a sustainable emotional contract around money between you and your partner.

You sit down with a counselor or financial therapist to figure out why you spend, why you save, and why you fight about it. This discipline is deeply rooted in psychology, often drawing heavily on the official academic clearinghouse that evaluates empirical links between core financial behaviors and relationship well-being.

Without that therapeutic layer, even the smartest financial plans collapse under stress.

Identify Unconscious Money Scripts

We all grow up absorbing beliefs about money from our parents.

These are your money scripts.

Maybe you were taught that money is scarce and must be hoarded. Maybe your partner grew up believing money is a tool for spontaneous enjoyment. When these two worldviews collide, the sparks fly. It makes total sense why 20% of romantic partners explicitly identify money as the single greatest challenge to their relationship continuity.

You have to drag these unconscious scripts out into the light.

Address Emotional Purchase Triggers

Spending is rarely just about acquiring an item.

Usually, it serves a deeper emotional purpose.

People spend to soothe anxiety, to exert control, or to compensate for financial imposter syndrome. A good financial counselor or psychotherapist specialising in money psychology will help you identify the specific feelings that trigger a trip to the mall or a massive late-night online shopping spree.

Integrate Behavioral Support Layers

Knowing how to save is easy. Actually doing it is brutal.

Couples routinely fail at money management because they ignore the underlying behavioral issues.

Some common pitfalls that derail otherwise healthy partnerships include:

- Attempting to fix complex financial trauma with a simple budgeting app.

- Treating the symptom of overspending without addressing the underlying emotional spending triggers.

- Failing to establish shared money routines, leaving one partner completely in the dark.

If your last attempt at budgeting ended in tears, you shouldn’t just give up. You just need a better support system.

Bridge Traditional Fiscal Gaps

A traditional financial advisor tells you where to put your cash. A family therapist asks about your childhood.

Financial counseling bridges that massive gap.

The physical relief is actually measurable. Clinical trials evaluating financial therapy models show a tangible biological impact on patients, dropping physiological muscle tenseness by 21% and acute money anxiousness by 22%.

How Affluent Partners Benefit From Wealth Programs

High-earning couples in the FatFire community face a very specific set of financial challenges.

They aren’t looking for tips on how to clip coupons or save fifty bucks on groceries.

They are desperately seeking alignment.

When your net worth scales rapidly, the weight of your financial decisions becomes incredibly heavy. A financial therapist helps these couples manage the psychology of abundance.

Build Shared Wealth Narratives

What is all this money actually for?

If one partner wants to retire at 40 and live on a sailboat, while the other wants to fund generational trusts and stay in their high-powered career, you have a massive problem. You must build a shared vision for your financial future.

Align On Abundance Psychology

Having a lot of money can bring an absurd amount of guilt and pressure.

Couples need a safe space to discuss how wealth impacts their identity. Sometimes, a financial marriage counseling session is the only place a high-earning individual feels comfortable admitting they are terrified of losing everything they built.

Determine Mutual Risk Tolerance

Investing isn’t just a numbers game.

It dictates whether or not you can sleep at night. If partners have wildly different risk tolerances, the financial stress will slowly eat away at the relationship.

| Partner Profile | Investment Mindset | Emotional Reaction to Market Dips |

|---|---|---|

| The Aggressive Builder | Highly tolerant of volatility, seeks maximum yield. | Views dips as a buying opportunity. Feels energized. |

| The Security Seeker | Prefers bonds and insured accounts, fears loss of capital. | Views dips as a catastrophic threat. Loses sleep. |

You have to find a middle ground that protects your assets and your sanity.

Establish Structured Routines For Fiscal Harmony

You need a practical blueprint to keep your financial lives running smoothly.

A two-month strategy works wonders for most couples looking to completely reset their money habits.

Audit Joint Money Beliefs

Spend your first month uncovering your financial backgrounds.

Sit down and share your deepest fears about debts and wealth. Be entirely honest about your financial situation.

Draft Shared Fiscal Covenants

Next, you need to create a literal document.

This is a simple written agreement outlining your mutual commitments to spending limits, savings goals, and honesty. It serves as your playbook for every major financial decision moving forward.

Schedule Routine Fiscal Reviews

You can’t just talk about money once a year and expect things to magically improve.

Set up a weekly check-in. Grab some coffee, sit down for twenty minutes, and review your spending. Then, hold a larger quarterly meeting to track your big financial goals.

Rebuild Mutual Trust After Monetary Conflicts

Trust is incredibly fragile.

And nothing shatters it quite like financial infidelity.

National data shows that 43% of people who combine finances admit to committing at least one act of financial infidelity against a partner.

Younger generations are particularly sensitive to this betrayal. Generational breakdowns reveal that 63% of Gen Z adults view financial lies as being just as destructive as physical cheating.

It rots a marriage from the inside out. Data collected on couples who explicitly choose to combine assets shows that 75% report that hidden purchases or bank lies directly degraded their relationship health.

Oddly enough, lying about money actually makes you poorer. Longitudinal field studies measuring actual bank account data established a direct correlation where high asymmetric financial deception between partners structurally predicts lower total household assets.

Resolve Hidden Debt Issues

Starting a life together with a mountain of hidden bills is a recipe for disaster.

Yet, 86% of couples married five years or less started their union with debt.

You have to put everything on the table. A financial counselor provides a neutral environment where you can confess your financial mistakes without the fear of immediate screaming or judgment.

Balance Unequal Income Dynamics

When one person makes significantly more than the other, resentment can quietly brew.

The higher earner might feel used. The lower earner might feel trapped or controlled. Therapy forces you to untangle your self-worth from your paycheck.

Protect Relationship Health With Clear External Boundaries

Money problems don’t always start inside the house.

Often, they walk right through the front door disguised as family or friends.

When your sibling asks for a $5,000 loan, how do you handle it? If you don’t have a strict, pre-agreed policy for dealing with external financial requests, you will end up fighting your partner over it.

You must establish rigid money boundaries with extended family and business partners to protect the core relationship.

Why Premarital Programs Prevent Future Marital Friction

You wouldn’t start a business with someone without signing a contract.

So why would you merge your entire financial life with someone without having a serious conversation first?

Premarital financial counseling is gaining massive traction for good reason. It merges values discovery with concrete, prenup-like agreements around spending and savings.

Peer-reviewed studies demonstrate that a short, structured three-session collaborative model effectively “primes” resistant couples, helping them safely untangle emotional baggage from numeric goals early on.

Get ahead of the problem.

How Practitioners Structure Affordable Program Tiers

Finding a good therapist can feel like hunting for a unicorn.

The field is still incredibly niche. While the U.S. has over 80,000 CFP professionals, the official regulatory body lists less than 50 elite, fully certified financial therapists nationwide.

Because of this scarcity, premium services can be painfully expensive.

Frankly, if you can’t afford a $400 emergency, dropping $200 an hour on a financial therapist sounds completely insane.

That is exactly why modern providers are introducing scalable models. Many successful practices now offer tiered pricing, 12-week intensive group programs, and sliding scale fees to make financial wellness accessible to people outside the top one percent.

FAQ

- Does financial counseling actually work? Yes. Established therapy data sets a baseline showing that roughly 70-75% of couples report significant improvements in relationship harmony and constructive communication patterns after professional counseling.

- How is this different from regular marriage counseling? Traditional marriage counseling focuses on general communication skills and emotional intimacy. Financial therapy explicitly tackles the mechanics of your money habits alongside the emotional weight of your financial decisions.

- When should a couple seek help? The moment financial disagreements escalate from mild annoyance to active deception or constant, draining arguments. Don’t wait until the bank accounts are entirely drained to ask for a lifeline.

Conclusion

Untangling your money issues takes an immense amount of hard work.

There are no shortcuts here.

You can’t just download a new budgeting app and expect years of deep-seated financial trauma and bad communication habits to magically vanish overnight.

You have to dig deep. You have to be vulnerable. You have to put your ego aside and look closely at the financial behaviors that are actively harming your partner.

But if you stay consistent and lean into the therapeutic process, your relationship has nowhere to go but up.

Keep having the hard conversations. Keep testing your new financial routines.

The peace of mind is absolutely worth the effort.